In April, Governor Kathy Hochul proposed a pied-a-terre tax on second homes in New York valued at $5 million. However, when the Department of Finance released an infographic detailing how much second homes would be taxed, it started at values of $1 million. How can that be?

The answer comes down to the homes' assessed tax value, as opposed to their actual sales value. This can be confusing to anyone who's looked at a New York City property tax bill and wondered how the city arrived at this valuation. Fortunately, in most cases, assessed tax values are much lower than current sales values; though depending on the market, the difference can vary greatly.

In this article:

In 2024, for example, a Manhattan penthouse that sold for $135 million had a market value—for tax purposes—of just $4.2 million. On the flip side, the difference between the market and sales values of homes in lower-income neighborhoods is often minor. So, how did we end up with a system that not only seems nonsensical but also unfair? This article explains how properties are valued for tax purposes and why the system is currently under scrutiny.

Market Value vs. Assessed Value

When it comes to property taxes, the most important distinction to understand is the one that distinguishes market value versus assessed value. Market value is the Department of Finance’s estimate of what the property would sell for under current market conditions. Assessed value is the number used to calculate property taxes.

In many U.S. cities and regions, market and assessed values are similar. In New York City, the assessed value varies because the city applies assessment ratios, which vary by property class, to each property. In addition, state law limits how quickly residential property taxes can rise. As a result, two homes with similar market values may have shockingly different assessed values—and, by extension, tax bills—depending on their classification and assessment history.

How Market Values and Assessed Values Are Calculated

A key factor in determining property values and, by extension, assessed tax values is the property’s class. In New York City, there are four classes of property:

- Class 1 includes one-, two-, and three-family homes, and very rarely exempt condos

- Class 2 includes cooperatives, condominiums, and rental buildings with more than three residential units

- Class 3 consists primarily of utility properties Class 4 includes commercial and industrial buildings, such as office towers, retail properties, hotels, warehouses, and factories.

The assessment methodology differs significantly across these categories, including between Class 1 and Class 2, even though both are residential. For Class 1, the property value is based on comparisons to other comparable home sales. For example, the assessment of a single-family home in Flushing, Queens, or Park Slope, Brooklyn, would be based on the recent sales of comparable homes in these neighborhoods. By contrast, in condos and co-ops, property values are based on the entire building, and specifically, on what the entire building would be worth if rented out (even though individual units are owned in these buildings). But this isn’t the only thing that determines how properties are ultimately assessed.

Class 1 assessments

Class 1 properties are assessed at 6 percent of their market value, so a $10 million townhouse would be valued at $600,000 for tax purposes. In addition, there are strict caps and phase-in rules—the assessed value of a class 1 property can’t increase more than 6 percent in a year, nor more than 20 percent over five years. This explains why many Park Slope brownstones, which were bought at modest prices in the 1990s but are now worth millions of dollars, are still taxed at rates that may seem more aligned with the property taxes paid on small condos in the Bronx or Queens.Class 2 condo assessments

Class 2 condo properties are treated differently in assessments. In the case of a $10 million luxury condo, for example, the city assigns a value based on what the unit would be worth if the entire condo was rented. Under this formula, a $10 million condo may be worth only $2.5 million. Even if assessed at $2.5 million, however, the city then applies a Class 2 assessment ratio of 45 percent to the unit, which further reduces the property’s assessed value to $1.115 million. What is notable here is the condo, while holding the same sales value as a $10 million townhouse, would end up with an assessed value that is nearly twice as high.Class 2 co-op assessments

While the assessment of condos and co-ops is similar, there is one major difference. In a condo, each owner receives a separate tax bill. In a co-op, the city sends a tax bill to the co-op, and the taxes are folded into shareholders’ fees. While this can complicated the ability to reduce property taxes based on specific situations, whether you’re in a condo or co-op, if a property is your primary residence, you are still eligible for additional property tax deductions, including STAR benefits, veterans’ exemptions, or senior benefits.

Why assessments matter

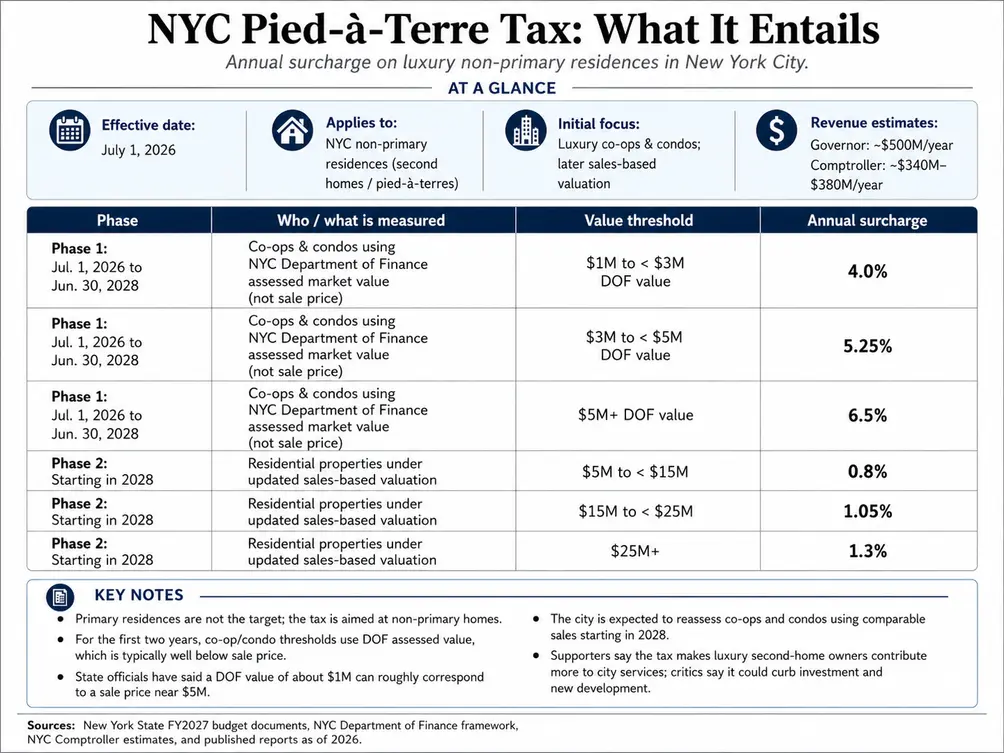

The pied-a-terre tax has called new attention to property assessments. Between July 1, 2026 to June 30, 2028, a temporary framework will be used to determine which pied-à-terre properties are subject to the new tax. In the initial phase, one- to three-family homes valued at more than $5 million will be taxed between 0.8 percent to 1.3 percent, depending on their Department of Finance-assessed value. Since most assessed values are well below sales values, it goes without saying that few one- to three-family homes will be impacted by this new law. By contrast, condo and co-op units with Department of Finance-assessed values of $1 million or more will be subject to the new tax, with rates between 4 percent and 6.5 percent. Most lawmakers assume this will mean that only condos that would sell for $5 million or more in the current market will be subject to the new tax.

Pied-a-terre tax details (New York Department of Finance)

Pied-a-terre tax details (New York Department of Finance)

Starting on July 1, 2028, and continuing until June 30, 2031, however, an entirely different valuation model will apply to all residential units. The key difference is that starting on July 1, 2028, condos and co-ops will no longer be valued based on a hypothetical scenario that treats them as potential rental units in a larger building but rather on the same basis as one- to three-family homes (that is, on their potential sales value). Under this model, all pied-à-terre properties with an assessed value exceeding $5 million will be subject to a tax of 0.8 percent to 1.3 percent, depending on their value.

At any time, property assessments directly affect the cost of living in New York City. They also can, at times, affect the ability of current owners to hold on to longstanding family homes.

Would you like to tour any of these properties?

Just complete the info below.

Or call us at (212) 755-5544

Still confused, or want to dispute your property's assessed value?

Property tax valuations in New York City are difficult to understand—so much so that the Department of Finance publishes a glossary of assessment-related terms on its website. Fortunately, the Department of Finance strives to be as transparent as possible and even offers an opportunity to contest assessments that seem unfair. If you want to challenge your assessed property value, visit the NYC Department of Finance. The deadline to dispute an assessed property value on a Class 1 property is March 15. For Class 2, 3, and 4 properties, you must file by March 1.

Select Open Houses Sunday, June 20, 2026

807 Riverside Drive, #1I

$445,000

Washington Heights | Condominium | 1 Bedroom, 1 Bath

Open House: Sunday, June 21, 2026

807 Riverside Drive, #1I (Douglas Elliman Real Estate -)

London Terrace Towers, #6I

$650,000

Chelsea | Cooperative | Studio, 1 Bath

Open House: Sunday, June 21, 2026

London Terrace Towers, #6I (Serhant)

Sutton55, #11F

$795,000

Midtown East | Cooperative | 1 Bedroom, 1 Bath | 825 ft2

Open House: Sunday, June 21, 2026

Sutton55, #11F (Next Stop NY)

328 West 86th Street, #PHA

$849,000

Riverside Dr./West End Ave. | Cooperative | 1 Bedroom, 1 Bath

Open House: Sunday, June 21, 2026

328 West 86th Street, #PHA (Compass)

The Kenilworth, #7C

$949,000

Carnegie Hill | Cooperative | 1 Bedroom, 1 Bath

Open House: Sunday, June 21, 2026

The Kenilworth, #7C (Douglas Elliman Real Estate -)

407 West 40th Street, #5A

$975,000

Midtown West | Cooperative | 2 Bedrooms, 2 Baths

Open House: Sunday, June 21, 2026

407 West 40th Street, #5A (Corcoran Group)

The Santa Monica, #4E

$975,000

Riverside Dr./West End Ave. | Cooperative | 2 Bedrooms, 1 Bath

Open House: Sunday, June 21, 2026

The Santa Monica, #4E (Compass)

The Elliot, #10G

$999,000

Riverside Dr./West End Ave. | Cooperative | 2 Bedrooms, 1 Bath

Open House: Sunday, June 21, 2026

The Elliot, #10G (Digs Realty Group LLC)

Sutton House, #3EB

$1,095,000

Beekman/Sutton Place | Cooperative | 2 Bedrooms, 2 Baths | 1,400 ft2

Open House: Sunday, June 21, 2026

Sutton House, #3EB (Stephen P Wald Real Estate Associates Inc)

11 Sterling Place, #5F

$1,450,000

Park Slope | Condominium | 2 Bedrooms, 1 Bath | 960 ft2

Open House: Sunday, June 21, 2026

11 Sterling Place, #5F (Brown Harris Stevens Brooklyn LLC)

Cannon Point North, #11M

$1,495,000 (-3.5%)

Beekman/Sutton Place | Cooperative | 2 Bedrooms, 2 Baths

Open House: Sunday, June 21, 2026

Cannon Point North, #11M (Compass)

305 West 86th Street, #4B

$1,500,000

Riverside Dr./West End Ave. | Cooperative | 2 Bedrooms, 2 Baths

Open House: Sunday, June 21, 2026

305 West 86th Street, #4B (Compass)

The New York Towers, #20B

$1,700,000

Gramercy Park | Cooperative | 2 Bedrooms, 1.5 Baths | 1,200 ft2

Open House: Sunday, June 21, 2026

The New York Towers, #20B (Nardoni Realty Inc)

The Clinton, #5B

$1,780,000

Riverside Dr./West End Ave. | Cooperative | 2 Bedrooms, 2 Baths

Open House: Sunday, June 21, 2026

The Clinton, #5B (Brown Harris Stevens Residential Sales LLC)

16 Wyckoff Street, #4

$1,795,000

Boerum Hill | Cooperative | 2 Bedrooms, 2 Baths

Open House: Sunday, June 21, 2026

16 Wyckoff Street, #4 (Compass)

CitySpire, #4103

$1,795,000 (-4.3%)

Midtown West | Condominium | 2 Bedrooms, 2.5 Baths | 1,172 ft2

Open House: Sunday, June 21, 2026

CitySpire, #4103 (Compass)

176 West 87th Street, #5C

$1,995,000

Broadway Corridor | Cooperative | 2 Bedrooms, 1.5 Baths

Open House: Sunday, June 21, 2026

176 West 87th Street, #5C (Compass)

Sheffield 57, #22S

$2,050,000

Midtown West | Condominium | 2 Bedrooms, 2 Baths | 1 ft2

Open House: Sunday, June 21, 2026

Sheffield 57, #22S (Brown Harris Stevens Residential Sales LLC)

230 Riverside Drive, #17D

$2,150,000

Riverside Dr./West End Ave. | Condominium | 3 Bedrooms, 2 Baths | 1,500 ft2

Open House: Sunday, June 21, 2026

230 Riverside Drive, #17D (Compass)

333 East 57th Street, #4A

$2,500,000

Midtown East | Cooperative | 4 Bedrooms, 4 Baths | 3,000 ft2

Open House: Sunday, June 21, 2026

333 East 57th Street, #4A (Corcoran Group)

799 Park Avenue, #8A

$4,200,000

Park/Fifth Ave. to 79th St. | Cooperative | 3 Bedrooms, 3 Baths

Open House: Sunday, June 21, 2026

799 Park Avenue, #8A (Douglas Elliman Real Estate -)

Would you like to tour any of these properties?

Just complete the info below.

Or call us at (212) 755-5544

Would you like to tour any of these properties?

Related Articles

Get To Know

Swim with a View: 30 Manhattan buildings with high-floor swimming pools and fitness centers

Today, June 20, 2026

Future New York

Top 10 condos in Turtle Bay and Beekman-Sutton Place + New developments and price-reduced listings

Thursday, June 11, 2026

Get To Know

Seven tips for getting past NYC's toughest co-op boards + Prewar gems with open houses

Friday, June 5, 2026

Get To Know

Pre-war vs. Post-war: Pros, cons, and featured listings

Wednesday, May 27, 2026

Get To Know

How historic districts impact property values and affordability + Charming NYC homes in landmarked properties

Tuesday, May 19, 2026

Future New York

See 20 Flatiron-style buildings and their availabilities as Landmarks tables "spaceship-like" addition in Meatpacking

Tuesday, May 12, 2026

Future New York

When, why, and how to hire a home inspector + Great new listings with outdoor space from $595K

Saturday, May 9, 2026

Great Listings

Top 10 Park Avenue buildings + Beautiful listings on New York's greatest residential boulevard

Thursday, May 7, 2026

Contributing Writer

Cait Etherington

Cait Etherington has over twenty years of experience working as a journalist and communications consultant. Her articles and reviews have been published in newspapers and magazines across the United States and internationally. An experienced financial writer, Cait is committed to exposing the human side of stories about contemporary business, banking and workplace relations. She also enjoys writing about trends, lifestyles and real estate in New York City where she lives with her family in a cozy apartment on the twentieth floor of a Manhattan high rise.