While the sticker shock of New York City apartments is well known, one lesser-known aspect is condo and co-op owners’ monthly carrying costs, which can sometimes be higher than their mortgage payments. However, New York City has several programs in place that can temporarily reduce real estate taxes, paid separately by condo owners and bundled into maintenance fees for co-op owners. Those who take advantage can save thousands of dollars a year in property taxes.

One overarching program for apartment owners is the New York City Cooperative and Condominium Tax Abatement, where managing agents or boards apply on behalf of the entire development and individual unit owners are required to meet certain eligibility requirements, namely that they use the apartment as their primary residence. Those that do qualify can receive a property tax reduction ranging from 17.5% to 28.1% a year (abatement based on assessed value of the units).

In this article:

It is important to note that a building is not eligible if it already benefits from a J-51 exemption, 420c, 421a, 421b, 421g, or any tax abatement program acquired by the sponsor, owner, or developer and passed on to the units within the building. The most well-known is the 421a tax exemption program, which was started in 1971 to encourage the development of underutilized or vacant property by dramatically reducing property taxes for a set amount of time. Developers who qualified could benefit from exemptions that usually lasted between 10 and 25 years, and the tax breaks were passed on to buyers of units within the building.

While 421a officially came to an end in January 2016, a revised version of the plan dubbed Affordable New York was released in January 2017. It offered tax incentives to buildings that reserved at least 20 percent of their units for affordable housing. Affordable New York expired in June 2022, and a replacement has not yet been announced, but its effects may still be seen in a handful of new buildings where the tax abatements remain in effect.

The 421-g Tax Incentive program was a real estate tax exemption and abatement for the conversion of commercial buildings, or portions of buildings, into multiple dwellings. It applied to areas of Lower Manhattan south of Murray Street, City Hall, and the Brooklyn Bridge. It was in effect at a time when many Financial District office buildings were being converted to offices; at a time when Midtown office conversions are being discussed, more information about the history of the exemption may be found here.

35 Woodhull Street #3 benefits from J-51 tax abatement (Compass)

35 Woodhull Street #3 benefits from J-51 tax abatement (Compass)

The J-51 property tax exemption program is granted to residential buildings (typically rent regulated) to encourage and subsidize renovations. According to the city’s website, a J-51 property tax exemption effectively freezes a building’s assessed value in its pre-renovated state. Thus the owner or shareholders do not have to pay the increase in property taxes caused by the increase in assessed value from the rehabilitation work. See the length and value of J-51 tax benefits here.

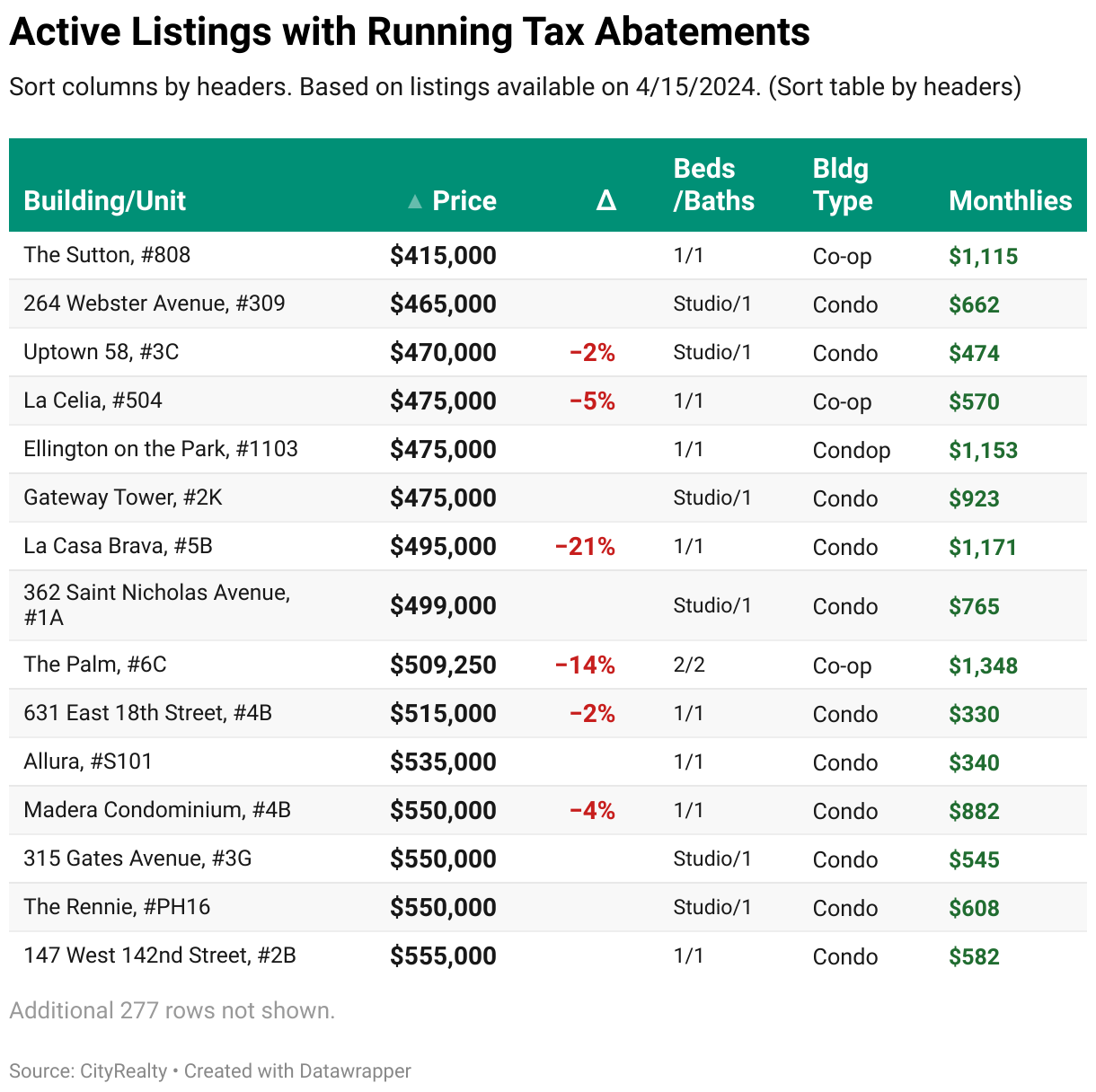

Select active listings with running tax abatements

Riverwalk Place, #5P (Corcoran Group)

501 Myrtle Avenue, #4B (Serhant LLC)

Hero LIC, #2G (Compass)

70-26 Queens Boulevard, #5A (Modern Spaces)

Would you like to tour any of these properties?

Just complete the info below.

Or call us at (212) 755-5544

Allura, #PHN603 (Compass)

Sofo Tower, #3D (Corcoran Group)

5th on the Park, #19D (Compass)

The Rennie, #614 (Brown Harris Stevens Development Marketing LLC)

Avalon Brooklyn Bay, #24B (Serhant LLC)

Atlantic Terrace, #8B (Compass)

The Lenox, #4B (Compass)

The Duet Condominium, #1A

$1,325,000 (-10.2%)

Gowanus | Condominium | 2 Bedrooms, 3 Baths | 1,465 ft2

The Duet Condominium, #1A (Compass)

Tiffany Tower, #2S (Compass)

Third + Bond, #1 (Compass)

35 Woodhull Street, #3 (Compass)

One Manhattan Square, #54D

$2,550,000

Lower East Side | Condominium | 2 Bedrooms, 2 Baths | 1,164 ft2

One Manhattan Square, #54D (EXP Realty NYC)

Circa Central Park, #2A (Reuveni LLC)

Schaefer Landing North, #4B (Douglas Elliman Real Estate)

70 Charlton, #4D (Brown Harris Stevens Residential Sales LLC)

400 Park Avenue South, #27C

$5,500,000

Flatiron/Union Square | Condominium | 3 Bedrooms, 3 Baths | 2,819 ft2

400 Park Avenue South, #27C (Corcoran Group)

On Prospect Park, #16S (Compass)

Would you like to tour any of these properties?

Just complete the info below.

Or call us at (212) 755-5544

Would you like to tour any of these properties?

Related Articles

Coney Island

Knicks in Five: 35 NYC condo and rental buildings with basketball courts

Thursday, June 18, 2026

Future New York

Making an Entrance: Top NYC Buildings with Porte-Cocheres and Dramatic Driveways

Wednesday, June 3, 2026

Future New York

Top 15 fitness centers in NYC condos as Radiant hits 60% sold and readies for move-ins

Friday, May 29, 2026

Great Listings

Easy Escapes: NYC apartments with private roof decks and cabanas under $2 million

Tuesday, May 26, 2026

Future New York

When, why, and how to hire a home inspector + Great new listings with outdoor space from $595K

Saturday, May 9, 2026

Future New York

Stay Flexible! 10 NYC condo buildings with dedicated Pilates rooms among wellness amenities

Friday, May 8, 2026

Future New York

Price Cuts: Bill Cosby's UES townhouse reduced by 14%; Palatial 5-bed at The Dakota now $5M off

Thursday, May 7, 2026

Get To Know