Like a miracle, in a sea of listings you discover a two bedroom that is not only under $600,000 but also under $300,000. Better yet, it’s in a desirable neighborhood, has recently been renovated and comes with a den, a large living room and an eat-in kitchen. What’s the catch? It is nearly certain that if you stumble across this or any similar listings, you are looking at an HDFC (Housing Development Fund Corporation) unit. While there are no hidden catches, purchasing an HDFC unit, if you even qualify, is a decision that should be given careful consideration.

In this article:

Qualifying for an HDFC Unit

First, there is the problem of qualifying. Unlike a typical co-op, to qualify, you may need to make less—rather than more—money. For example, if you’re a family of four and your declared household income is greater than $150,000 annually, you will likely not qualify for most HDFC units currently on the market. Ironically, this means that a family struggling to qualify to rent an average-priced two-bedroom apartment under the “40-x-the-monthly-rent” rule makes too much money to qualify for most HDFC purchases.More surprising to many would-be HDFC buyers is what one is expected to bring to the table. Like most co-ops, HDFC co-ops require at least 20 percent down. This means that first-time buyer mortgages, which frequently require only 3 percent to 5 percent down, are out of the question. But cash-strapped HDFC co-ops often require much higher down payments and even seek cash-only deals. In other words, in order to buy into a HDFC building, you will need to be income poor but asset rich.

If you are among the rare breed of New Yorker who qualifies for an HDFC unit, you will be among the lucky few who have the option of purchasing an apartment well under market value. Whether or not it is a strategic purchase in the short- or long-term, however, is another question.

1212 Ocean Avenue, #5B (Corcoran Group)

Reasons to Buy an HDFC Unit

If you do qualify for an HDFC unit, the short- and long-term gains can be significant. Since the units are usually, but not always, well below market value, your mortgage will likely carry for much less than current market rent on a similar unit. In addition, most HDFC units, which were created to provide affordable housing to people living on low to middle incomes, have relatively low maintenance fees (usually ranging from $300 to $650 monthly). Again, this means significantly lower monthly costs. If so inclined, this also means having more money on hand to invest in one’s unit. As a result, even a unit that requires a gut renovation—and many HDFC units do—may turn out to be a strategic purchase.Of course, much depends on whether or not you plan to stay for decades or simply for a few years. If you’re buying an HDFC unit with the intention of staying for decades, you’re likely making a great decision. If the unit is located in a co-op with solid financials and it otherwise meets your criteria in terms of space and location, you will save thousands of dollars on housing every year and more importantly, you’ll own in a market where owning can be a challenge, even for fully employed professionals. By contrast, if you plan to move, an HDFC unit may turn out to be an investment you live to regret.

Reasons to Avoid Buying an HDFC Unit

Buying real estate in New York City is nearly always a great long-term investment. The one exception to this rule is the purchase of an HDFC unit. While HDFC units are increasingly experiencing bidding wars and in some instances, even being sold at or close to market value, they are also subject to restrictions that work in the favor of co-ops rather than sellers.

Most notably, HDFC co-ops impose a high flip tax on sales. Typically, 30 percent of a seller’s profits are kicked back to the co-op at the time of the sale. In some buildings, however, the flip tax can be as high as 50 percent. Depending on the co-op, exceptionally high flip taxes may apply to all sellers or only to those who choose to sell after owning for a short period of time (e.g., less than five years). Thus, while HDFC units are frequently sold at a profit (bear in mind that many of these units were originally purchased from the City for a mere $250—yes, $250—so making a profit is inevitable), as a rule, it is never advisable to purchase an HDFC if your ultimate goal is to sell the unit at a profit.

High flip taxes are not the only downside to HDFC purchases. While some HDFC buildings resemble well-managed market-rate co-ops, others have suffered from years of poor management and neglected maintenance. Before purchasing an HDFC unit, you are advised to research the building’s financial history and to investigate whether or not the building has any recent safety or maintenance violations on record. While no one welcomes maintenance fee increases, in HDFC buildings tenants often face the opposite problem. After all, in buildings where many or most residents are living on fixed incomes, keeping maintenance fees low is often considered a greater priority than addressing major building repairs. As a result, one may end up owning their dream apartment but in a building with compromised conditions, and this can impact one’s quality of life, as well as the value of their investment.

High flip taxes are not the only downside to HDFC purchases. While some HDFC buildings resemble well-managed market-rate co-ops, others have suffered from years of poor management and neglected maintenance. Before purchasing an HDFC unit, you are advised to research the building’s financial history and to investigate whether or not the building has any recent safety or maintenance violations on record. While no one welcomes maintenance fee increases, in HDFC buildings tenants often face the opposite problem. After all, in buildings where many or most residents are living on fixed incomes, keeping maintenance fees low is often considered a greater priority than addressing major building repairs. As a result, one may end up owning their dream apartment but in a building with compromised conditions, and this can impact one’s quality of life, as well as the value of their investment.

Finally, while you may not be planning to move, you can’t always anticipate when and why you will need to move for work or personal reasons. Again, on this account, HDFC units pose unique risks. As already noted, only a small percentage of New Yorkers qualify for HDFC units and cash-strapped HDFC co-ops are frequently looking for buyers with large down payments and even for cash-only deals. This means that HDFC units often sit on the market for weeks and even months longer than units in non-HDFC buildings. To make matters worse, most HDFC co-ops also place restrictions on rentals. This means that in addition to waiting longer than usual to turn over a unit, you may find yourself unable to rent out your unit while waiting to sell.

While there is no reason to avoid purchasing an HDFC unit, it’s by no means recommended for serial movers or buyers hoping to profit from their real estate investments in the short term. With HDFC purchases, the return on investment is something typically only realized in decades, not years.

While there is no reason to avoid purchasing an HDFC unit, it’s by no means recommended for serial movers or buyers hoping to profit from their real estate investments in the short term. With HDFC purchases, the return on investment is something typically only realized in decades, not years.

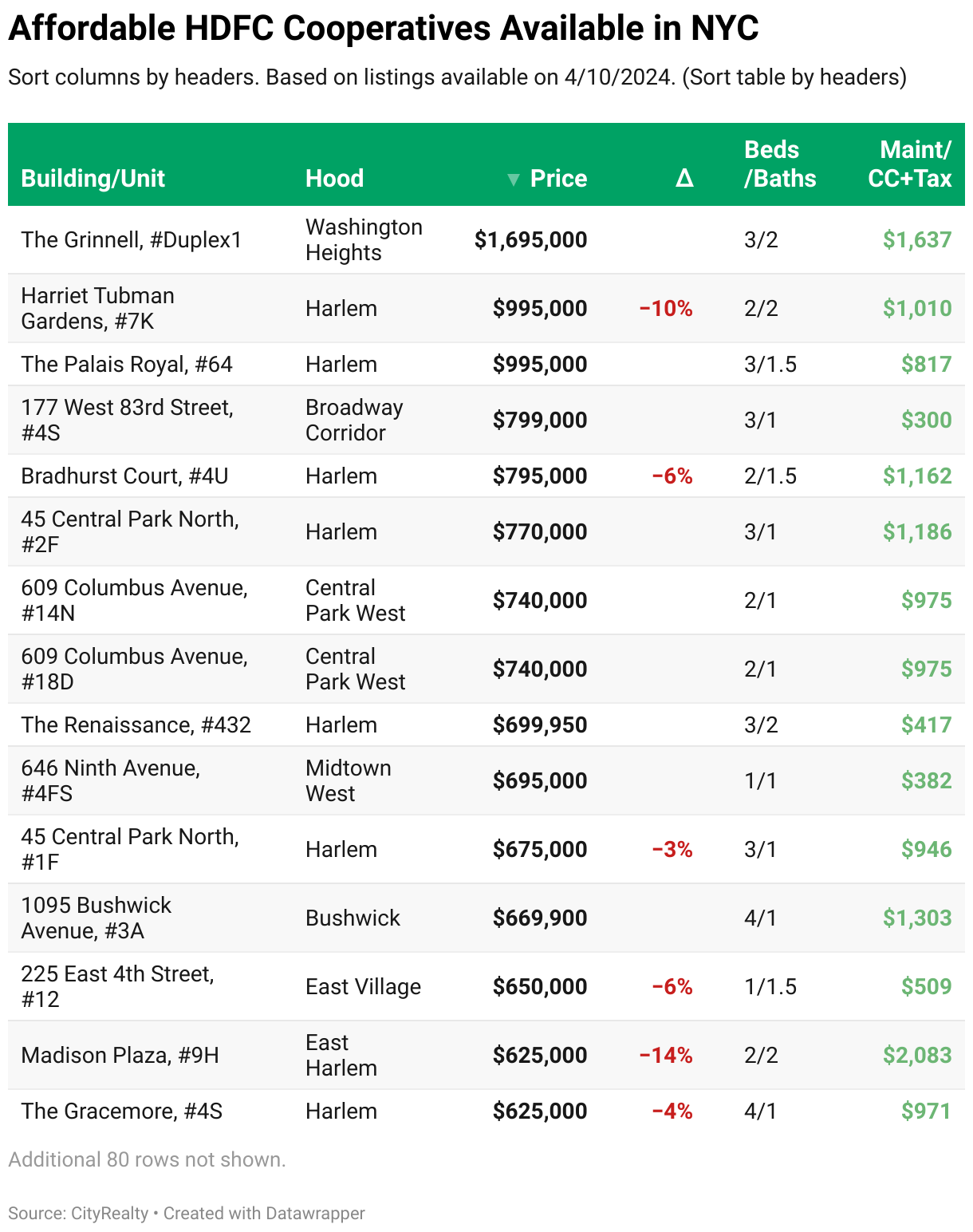

Recently-listed HDFC apartments around NYC

237 Hancock Street, #11 (Brown Harris Stevens Brooklyn LLC)

Site Five Cooperative, #2W (Sothebys International Realty)

The Cranmoor, #5C (Douglas Elliman Real Estate)

1513 Lexington Avenue, #4S (Sothebys International Realty)

342 East 100th Street, #4D (Compass)

225 East 4th Street, #12 (Brown Harris Stevens Residential Sales LLC)

160 East 2nd Street, #3BB (Brown Harris Stevens Residential Sales LLC)

409 Edgecombe Avenue, #10G (Bizzarro Agency LLC)

211 West 144th Street, #6A (Keller Williams NYC)

307 West 153rd Street, #11 (Corcoran Group)

168 Lenox Avenue, #1A (Brown Harris Stevens Residential Sales LLC)

The Townsend, #1A (Brown Harris Stevens Residential Sales LLC)

219 West 144th Street, #34 (Bizzarro Agency LLC)

1400 on Fifth, #3L (Sothebys International Realty)

108 West 114th Street, #4B (Serhant)

The Victor Hugo, #40 (Akam Sales & Brokerage Inc)

585 West 214th Street, #6D (Douglas Elliman Real Estate)

237 Eldridge Street, #34 (Corcoran Group)

200 Claremont Avenue, #25

$595,000

Morningside Heights | Cooperative | 3 Bedrooms, 1 Bath | 1,070 ft2

200 Claremont Avenue, #25 (Sothebys International Realty)

175 Claremont Avenue, #32 (Corcoran Group)

Westview, #315 (Compass)

15 Fort Washington Avenue, #6E

$333,000

Washington Heights | Cooperative | 1 Bedroom, 1 Bath | 690 ft2

15 Fort Washington Avenue, #6E (Corcoran Group)

Related Articles

Future New York

When, why, and how to hire a home inspector + Great new listings with outdoor space from $595K

Saturday, May 9, 2026

Get To Know

When, why, and how to buy or co-buy an apartment for a child + Listings under $500K with flexible purchasing options

Tuesday, April 28, 2026

Future New York

What is a maisonette? See 25 beautiful examples from $600K of NYC townhouse living without compromise

Tuesday, April 14, 2026

Get To Know

HDFC Co-ops: NYC's most and least affordable housing option + Open lotteries and new listings from $149K

Wednesday, April 1, 2026

Get To Know

How property values are assessed in NYC + Great new listings with open houses from $445K

Saturday, June 20, 2026

Get To Know

Swim with a View: 30 Manhattan buildings with high-floor swimming pools and fitness centers

Saturday, June 20, 2026

Future New York

What's old is new again: Mass timber construction in NYC as Timberburg readies to launch sales

Tuesday, June 16, 2026

Get To Know

What New York’s transparency bill could mean for whisper listings + Public listings with open houses

Friday, June 12, 2026

Contributing Writer

Cait Etherington

Cait Etherington has over twenty years of experience working as a journalist and communications consultant. Her articles and reviews have been published in newspapers and magazines across the United States and internationally. An experienced financial writer, Cait is committed to exposing the human side of stories about contemporary business, banking and workplace relations. She also enjoys writing about trends, lifestyles and real estate in New York City where she lives with her family in a cozy apartment on the twentieth floor of a Manhattan high rise.