Market Insight

In April, Governor Kathy Hochul proposed a pied-a-terre tax on second homes in New York valued at $5 million. However, when the Department of Finance released an infographic detailing how much second homes would be taxed, it started at values of $1 million. How can that be?

Last week, Mayor Zohran Kwame Mamdani and NYC Parks Commissioner Tricia Shimamura announced the opening of registration for free Learn to Swim classes across New York City that will teach young people aged 18 months to 17 years old how to swim and build water safety skills. The classes will take ...

A decade ago, the glass curtain wall seemed to be the default language of new construction in New York. It still has its place, especially in office towers where transparency, skyline views, and bringing natural light to deeper open floor plates remain highly marketable. But in residential archit...

Type

Bedrooms

Avg / Median

Currency

Pricing based on the past 12 month sales

Buildings

In the first quarter of 2026, Manhattan’s apartment contracts totaled $6,906,075,016 in ask volume across over 2,500 deals, with the average asking price coming in at $2.681M and an average of $1,709 per square foot. The buildings that accounted for the most activity tend to follow a familiar pa...

The New York Knicks have been described as the only sports team that brings New York City together, as opposed to divisions between Yankees/Mets and Jets/Giants fans, and the entire city seems unified in celebrating the Knicks' first NBA championship in 53 years. The team was honored with the fir...

From June 9-15, 2026, over 300 condos, co-ops, condops, and townhouses in core New York City areas experienced price reductions, a noticeable week-over-week decrease. This comes at a time when CityRealty data shows that average Manhattan condo prices are nearing record highs, and Manhattan co-ops...

Pre-leasing is underway at Willow House, an eight-story mixed-use building located at 1404 Willow Avenue, on the corner of 14th Street in Hoboken's North End. Rents start at $3,400/month for studios, $4,300/month for one-beds, $5,985/month for two-beds, $8,200/month for three-beds, and $17,000/mo...

From June 8-14, 2026, 277 residential contracts were signed in Manhattan. This is a small week-over-week increase, but was 57 more contracts than were signed the same week in 2025. Contract activity typically slows in June following strong volume in April and May, but 2026 could be the strongest ...

In loft buildings dating back to the mid-19th century, exposed timber columns, joists, and ceiling beams add a note of historic charm to a converted home. But between new building techniques, a rise in popularity, and revised building codes, a number of 21st century buildings are coming to embrac...

On the week ending June 13, 2026, 218 residential apartment sales were recorded in Manhattan, holding steady week over week. Four of the five highest-priced sales were for homes with views of Central Park West, and located no less than one block from "New York's backyard."

What New York’s transparency bill could mean for whisper listings + Public listings with open houses

A stack of bills awaiting Governor Kathy Hochul’s signature includes the “Fair and Transparent Real Estate Listings Act,” a measure that would make public marketing the default for residential sale and rental listings in New York State. The bill does not eliminate private listings outright, but i...

Manhattan’s luxury housing market is already subject to mansion taxes and transfer taxes. As of July 1, 2026, the luxury market will be subject to another tax—New York’s pied-à-terre tax on second homes.

From June 2-8, 2026, nearly 450 condos, co-ops, condops, and townhouses experienced price reductions. This is a noticeable week-over-week spike in the number of price reductions; however, the vast majority of cuts were small reductions below 10 percent, possibly aimed at drawing attention to a li...

More In Market Insight

-

6sqft (our blog)

- From Policy NYC Council to hold hearing on Ryder’s Law after fatal Central Park horse-drawn carriage accident

- From Distinctive Homes For $1.6M, this Connecticut estate has an art studio, guest house, pool, and a vintage modern vibe

- From Affordable Housing 1,000-unit affordable and supportive housing project breaks ground in East Flatbush

- From Policy NY attorney general sues Brooklyn landlords for overcharging rent-stabilized tenants

- From Policy Knicks-themed Penn Station subway entrance will stay orange and blue through next season

-

Get To Know

- From Get To Know How property values are assessed in NYC + Great new listings with open houses from $445K Saturday, June 20, 2026

- From Get To Know Swim with a View: 30 Manhattan buildings with high-floor swimming pools and fitness centers Saturday, June 20, 2026

- From Get To Know What's old is new again: Mass timber construction in NYC as Timberburg readies to launch sales Tuesday, June 16, 2026

- From Get To Know What New York’s transparency bill could mean for whisper listings + Public listings with open houses Friday, June 12, 2026

- From Get To Know What the pied-à-terre tax could mean for Manhattan prices + NYC penthouse listings from $499K Friday, June 12, 2026

-

Rental Building News and Offers

- From Coney Island Knicks in Five: 35 NYC condo and rental buildings with basketball courts Thursday, June 18, 2026

- From New Jersey Willow House: Boutique rental in Hoboken's resurgent North End launches with two months free rent Thursday, June 18, 2026

- From Midtown East New developments in Murray Hill as Midtown prepares for influx office-to-residential conversions Thursday, March 12, 2026

- From Turtle Bay/United Nations Anagram Turtle Bay debuts “Residences From The Top” with skyline views and a half-month free rent Friday, March 6, 2026

- From Long Island City TF Cornerstone's waterfront rental tower is leasing from $3,295/month + One month free rent Thursday, March 5, 2026

-

Market Reports & Research

- From New Developments Top-selling NYC buildings and priciest contracts of Q1 2026 Wednesday, April 8, 2026

- From Annual Market Reports NYC’s top-selling buildings of 2025 as Downtown deals reach new highs Friday, January 2, 2026

- From Monthly Market Reports NYC’s top-selling buildings: Downtown deals drive Q3 2025 as outer boroughs gain ground Wednesday, October 29, 2025

- From Monthly Market Reports Manhattan’s market held firm this summer, except in these price-dropping neighborhoods Friday, October 10, 2025

- From New Developments NYC's best-selling residential buildings of 2025 and their availabilities Wednesday, July 23, 2025

-

Great Listings

- From Great Listings How property values are assessed in NYC + Great new listings with open houses from $445K Saturday, June 20, 2026

- From Great Listings Swim with a View: 30 Manhattan buildings with high-floor swimming pools and fitness centers Saturday, June 20, 2026

- From Great Listings Knicks in Five: 35 NYC condo and rental buildings with basketball courts Thursday, June 18, 2026

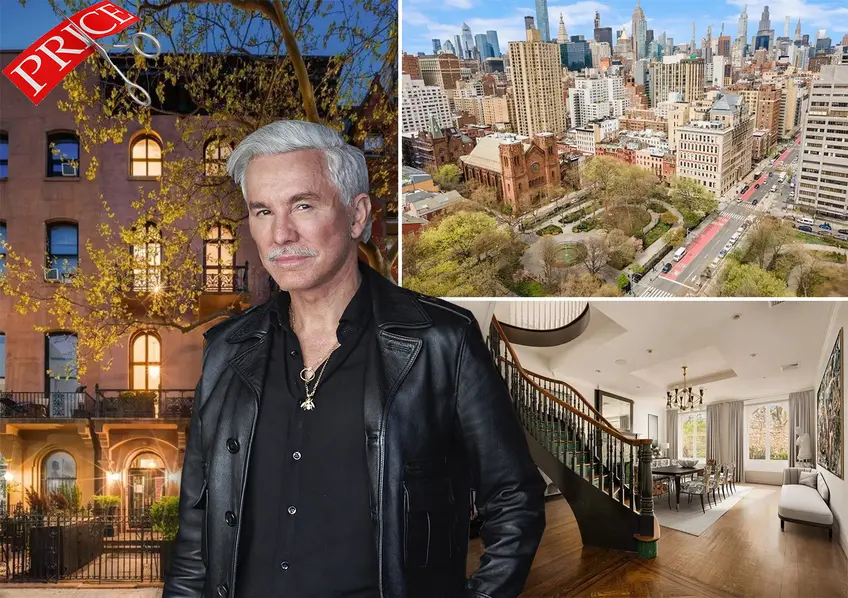

- From Great Listings Price Cuts: Baz Luhrmann’s Gramercy townhouse slashed by $7M; New discounts at Brooklyn and Queens’ tallest towers Thursday, June 18, 2026

- From Great Listings Willow House: Boutique rental in Hoboken's resurgent North End launches with two months free rent Thursday, June 18, 2026

-

Carter's View

- From In The Details Where buildings meet the sky: The return of the cornice, from Fifth Avenue to Lispenard Street Wednesday, April 15, 2026

- From In The Details NYC Brutalism: The good, the bad, and the ugly Thursday, May 15, 2025

- From Behind The Buildings One Hundred Barclay: A Monument of American Progress in Architecture Friday, January 3, 2025

- From In The Details Iconic NYC Holiday Locations Tuesday, December 24, 2024

- From Behind The Buildings As the Waldorf Astoria prepares for new chapter, revisit the legendary history of Manhattan's greatest Art Deco hotel Tuesday, December 17, 2024